New York offers some of the most generous Medicaid coverage in America, especially for seniors needing long-term care.

If you’re wondering whether you qualify for Medicaid in New York in 2026, this guide breaks down the exact income and asset limits, plus a major upcoming change that could affect your eligibility for home care services.

Page Contents

- 1 Key Takeaways for 2026

- 2 New York Medicaid Income Limits 2026

- 3 New York Medicaid Asset Limits 2026

- 4 The 30-Month Look-Back Period: What You Need to Know

- 5 Income and Asset Comparison: New York vs. Federal Baseline

- 6 How to Apply for New York Medicaid

- 7 Planning Steps Before the Look-Back Takes Effect

- 8 Who Should Consider Medicaid Planning?

- 9 New York Medicaid FAQs (2026)

- 9.1 1. What are the 2026 income limits for New York Medicaid?

- 9.2 2. How much in savings can I keep for New York Medicaid?

- 9.3 3. Will my house count against Medicaid limits?

- 9.4 4. What happens if my income is too high?

- 9.5 5. Does New York check my money transfers before approving me?

- 9.6 6. What can my healthy spouse keep if I’m on Medicaid?

- 10 Where to Get Help

Key Takeaways for 2026

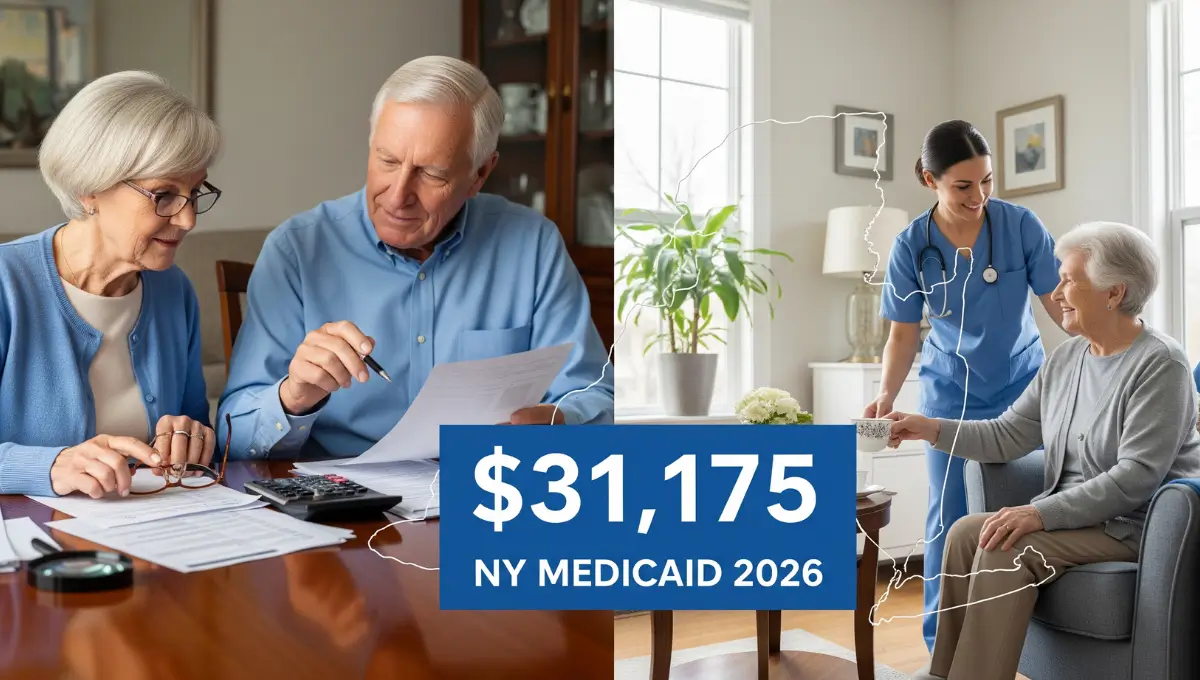

- Single individuals can have up to $31,175 in assets and still qualify for institutional Medicaid

- Married couples can protect up to $154,140 in assets when one spouse needs nursing home care

- Income limits vary by program: $1,732/month for nursing home care, higher limits for Community Medicaid

- Major change coming: A 30-month look-back period will soon apply to Community Medicaid (home care services)

- New York’s limits are significantly higher than most other states

New York Medicaid Income Limits 2026

Nursing Home Medicaid (Institutional Care)

Monthly income limit: $1,732 for a single person

If your income exceeds this amount, you can still qualify through a Miller Trust (Income Trust). New York allows you to “spend down” excess income on medical expenses.

Community Medicaid (Home Care Services)

Monthly income limit: Approximately $1,732 (subject to regional variation)

Community Medicaid covers home health aides, personal care services, and adult day care so you can stay in your home instead of entering a nursing home.

Medicaid Managed Long-Term Care (MLTC)

Similar income rules apply, but you must need nursing home-level care to qualify for managed long-term care services at home.

New York Medicaid Asset Limits 2026

For Single Individuals

Countable asset limit: $31,175

This is what you can own and still qualify. Your home, one car, personal belongings, and certain other items don’t count toward this limit.

For Married Couples (Spousal Impoverishment Rules)

When one spouse needs nursing home care:

- Community Spouse Resource Allowance (CSRA): Up to $154,140

- Minimum CSRA: $29,724

This means the healthy spouse can keep between $29,724 and $154,140 in assets while their partner qualifies for Medicaid.

What Assets Don’t Count?

- Your primary home (with equity up to $1,071,000 in 2026)

- One vehicle

- Personal belongings and household items

- Prepaid burial plots and irrevocable funeral trusts

- Small amounts of life insurance (face value under $1,500)

The 30-Month Look-Back Period: What You Need to Know

Current Rules (Through 2026)

Right now, New York only applies a look-back period to nursing home Medicaid, not home care services. This means you can transfer assets and immediately qualify for Community Medicaid.

Coming Change

New York will implement a 30-month look-back period for Community Medicaid. This means:

- Medicaid will review all asset transfers made in the 30 months before you apply for home care

- If you gave away assets during this time, you may face a penalty period where you’re ineligible for coverage

- The exact implementation date is still pending but expected in 2026

Why This Matters

If you anticipate needing home care services in the near future, the window to transfer assets without penalties is closing. After the look-back takes effect, any gifts or transfers could delay your eligibility.

Income and Asset Comparison: New York vs. Federal Baseline

| Category | New York 2026 | Federal Baseline | Difference |

|---|---|---|---|

| Individual asset limit | $31,175 | $2,000 | +$29,175 |

| Couple asset limit | $154,140 | $3,000 | +$151,140 |

| Home equity limit | $1,071,000 | $713,000 | +$358,000 |

New York’s limits are dramatically higher, making coverage accessible to middle-class families who would be disqualified in most other states.

How to Apply for New York Medicaid

- Contact your local Department of Social Services (DSS) or apply online through NY State of Health

- Gather documentation: proof of income, bank statements, property deeds, insurance policies

- Complete a medical needs assessment if applying for long-term care services

- Submit your application and respond to any requests for additional information

Processing typically takes 45-90 days for long-term care applications.

Planning Steps Before the Look-Back Takes Effect

If you or a loved one may need home care services:

Act now: Consult with a Medicaid planning attorney or certified Medicaid planner before the 30-month look-back is implemented

Review your assets: Identify which assets are countable and which are exempt

Consider legal protections: Irrevocable trusts, spousal transfers, and other strategies can protect assets while maintaining eligibility

Don’t wait: Once the look-back period begins, transfers made today could affect your eligibility for 2.5 years

Who Should Consider Medicaid Planning?

- Adults over 60 with chronic health conditions

- Anyone diagnosed with Alzheimer’s or dementia

- Individuals who have had strokes or mobility issues

- Middle-class families with assets above the limits

- Married couples where one spouse needs care

Professional planning can help you qualify for benefits while protecting your life savings for your spouse and heirs.

New York Medicaid FAQs (2026)

1. What are the 2026 income limits for New York Medicaid?

2. How much in savings can I keep for New York Medicaid?

3. Will my house count against Medicaid limits?

4. What happens if my income is too high?

5. Does New York check my money transfers before approving me?

6. What can my healthy spouse keep if I’m on Medicaid?

Where to Get Help

- Local Department of Social Services: Find your county office at nyc.gov or your county website

- NY State of Health: info.nystateofhealth.ny.gov (official health insurance marketplace)

- Elder law attorneys: Specialize in Medicaid planning and asset protection

- Certified Medicaid planners: Can guide you through the application process

Disclaimer: This information reflects official government data as of January 5, 2026. New York Medicaid eligibility is complex and depends on your individual circumstances, including medical need assessments, income verification, and asset evaluations. Always verify current eligibility with your local Department of Social Services and consider consulting with a Medicaid planning professional or elder law attorney for personalized guidance before applying.